The Flexographic Technical Association of South Africa (FTASA) hosted the Gauteng Flexo Frontier 2026 seminar, in partnership with Printing SA, on 18 February at the Protea Hotel in Kempton Park. Jermaine Naicker, Managing Director at Printing SA, spoke about the state of the printing industry in 2026.

Naicker presented a data-led assessment of South Africa’s printing and packaging industry, outlining employment contraction, market rebalancing, substrate shifts and the structural rise of packaging, alongside a detailed response plan to address mounting skills shortages.

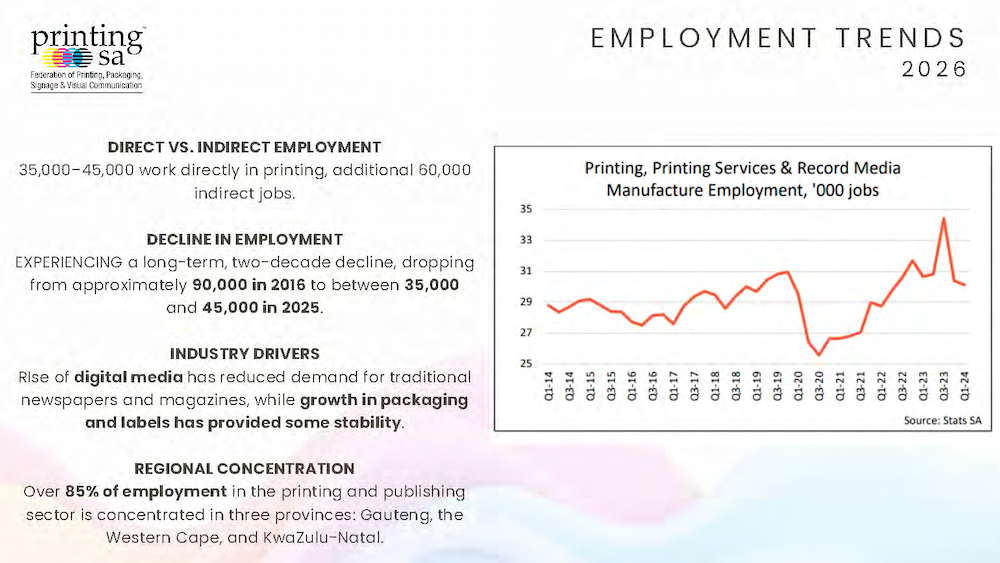

Industry employment has declined significantly over the past decade, falling from approximately 90,000 jobs in 2016 to between 30,000 and 35,000 today. The contraction accelerated through digital media substitution in publishing, compounded by COVID-19 disruption, rising imports and prolonged economic pressure. However, packaging and labels have cushioned the decline, providing relative stability within an otherwise shrinking employment base. The industry remains regionally concentrated, with KwaZulu-Natal, Gauteng and the Western Cape accounting for 85% of total jobs.

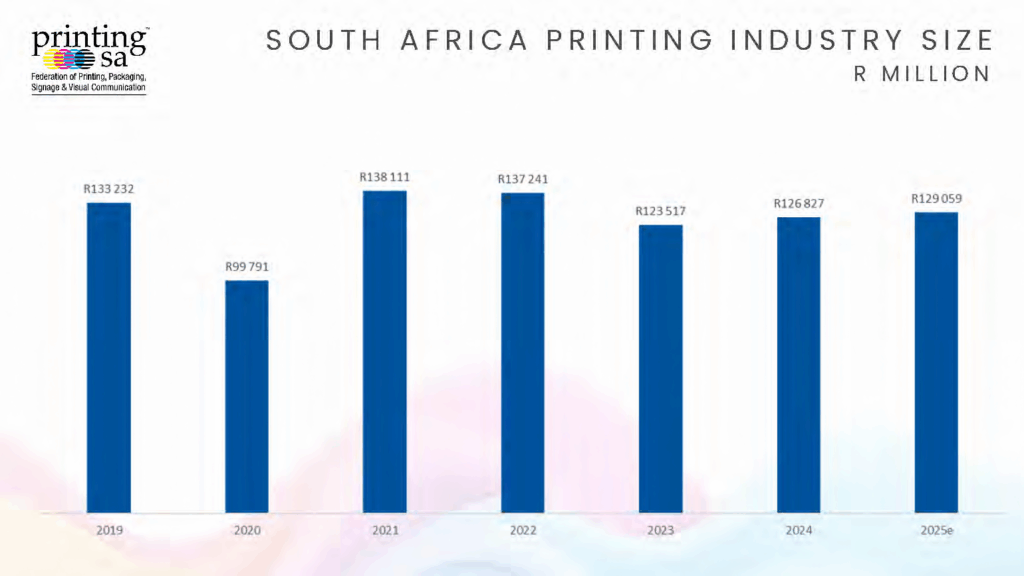

Market value trends reflect volatility followed by correction. The industry was valued at R133 billion in 2019 before experiencing a sharp pandemic-related decline in 2020. A strong rebound in 2021 and 2022 pushed values above pre-COVID levels, but the market has since entered a normalisation phase, with 2025 estimated at R129 billion. Forecast growth to 2030 sits at 1.9% annually, driven by inflation rather than real volume expansion. Print volumes are projected to decline by between 1.1% and 3.9%, reinforcing that revenue stability will not equate to output growth.

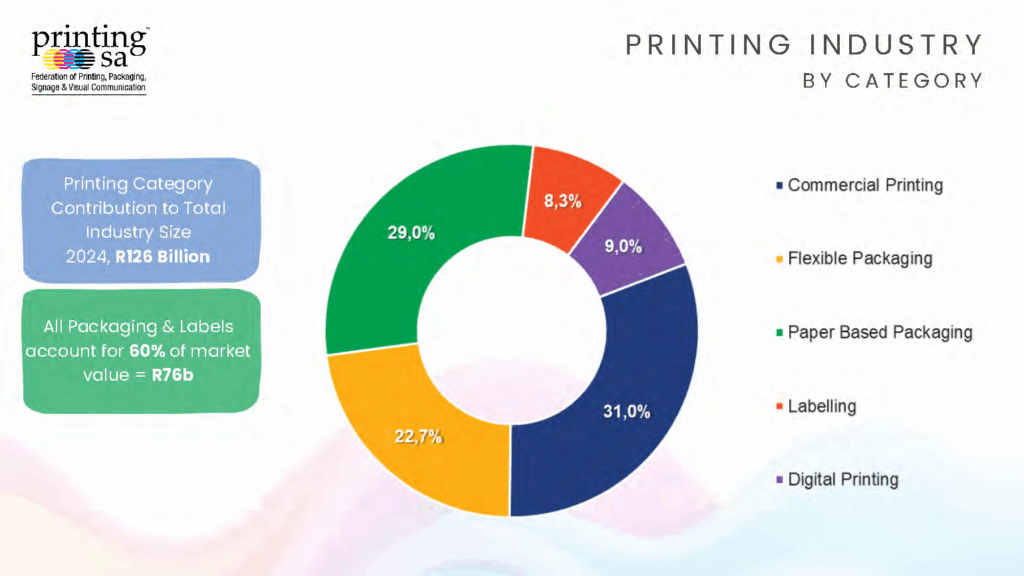

Segment analysis confirms a structural shift toward packaging. While commercial printing remains the single largest standalone segment at 31% of market share, flexible packaging, paper-based packaging and labelling collectively account for 60% of industry value, approximately R76 billion. Commercial print contributes R39 billion, paper-based packaging approximately R36–37 billion, flexible packaging R28–29 billion, digital printing R11.3 billion and labelling R10.5 billion. The data positions packaging and labels as the dominant economic drivers of the sector.

Substrate consumption trends underscore this shift. Paper usage has fallen from 759,000 tons in 2019 to an estimated 580,000 tons in 2024, reflecting structural demand erosion and import pressure. Plastic consumption, by contrast, has remained stable, moving marginally from 490,000 tons pre-COVID to 486,000 tons in 2024, making it the most consistent converting substrate in the market. Paper products remain the most exposed to import competition.

The industry’s contribution to GDP has gradually declined from approximately 2% in 2016 to 1.7% in 2024, indicating a slow structural contraction rather than abrupt collapse. This marginal but consistent reduction mirrors employment and volume trends across the sector.

Operational pressures are reshaping business models. Retailers are increasingly shifting slower-moving brands into just-in-time supply arrangements to protect margins and reduce inventory exposure, transferring risk and cash-flow strain downstream to converters. Automation investment continues as firms pursue cost containment and operational efficiency. E-commerce growth remains a packaging driver, reinforced by the 2024 South African market entry of Amazon, which has increased demand for paper-based packaging and labelling. Concurrently, mergers and acquisitions are accelerating as companies consolidate to reduce overheads and strengthen competitive positioning.

Global context reinforces the packaging narrative. The worldwide packaging market, valued at $512 billion in 2024, is forecast to reach $695 billion by 2029, reflecting a 6.3% compound annual growth. Flexographic printing alone accounted for $230 billion in 2024 and is projected to grow in line with broader packaging demand. Growth is underpinned by FMCG resilience, logistics expansion and sustained brand investment in corrugated, flexible packaging and labels.

Against this backdrop, Naicker identified the industry’s most acute structural risk: deteriorating skills capacity. Mechanical aptitude benchmarks indicate declining competency levels, youth interest in technical trades is weakening, practical training infrastructure is limited and labour costs continue to rise. Colour perception assessments have also revealed recurring deficiencies, highlighting technical competency concerns at operator level.

In response, Printing SA has shifted toward targeted, industry-specific training interventions rather than relying solely on traditional apprenticeship pathways. The association is pursuing regional centres of excellence to provide practical training environments and has established partnerships with TVET colleges to leverage existing infrastructure for print-focused skills development.

A central intervention is the full funding of 20 apprentices through a three-year programme at a total investment of R6 million, equating to approximately R300,000 per apprentice. This model pairs Printing SA with participating businesses to carry apprentices through to trade test qualification, representing a direct financial commitment to rebuilding the skills pipeline.

Training pathways span pre-press, flexographic machine operation, corrugated board production, carton manufacturing and bag-making, with additional short courses tailored to flexible packaging operations. Leadership and management development programmes are also in place, alongside a revised print estimator qualification to modernise commercial competency.

Recognising the digital shift within packaging and labels, Printing SA is expanding commercial digital printing programmes and developing flexographic-focused digital qualifications. Software training through partnerships includes Adobe certifications, while new offerings in artificial intelligence, generative AI for graphic design and business-support tools aim to future-proof technical capability.

The overarching outlook presented is one of stabilisation rather than expansion. The industry appears to have passed its deepest contraction cycle and is rebalancing within an inflation-supported revenue environment. Volume pressures will persist, but packaging and labels remain structurally resilient. The decisive variable for long-term sustainability, Naicker concluded, will be the industry’s ability to rebuild and modernise its skills base while consolidating operational efficiency in a non-growth market.

PRINTING SA

+27 11 287 1160

info@printingsa.org

http://www.printingsa.org